Back in October, R. R. Reno, editor-in-chief of First Things, published a manifesto revoking, or at least greatly qualifying, the approval of free-market capitalism offered by Richard John Neuhaus, Michael Novak, and the other luminaries who made First Things an intellectual force. As may well be expected, this has occasioned strong rejoinders from Samuel Gregg, Michael Uhlmann, and others.

I delayed responding to Reno, in part because Reno and I had already gone back and forth on some of these questions, and in part because I found it difficult to make out just what Reno is saying. His piece is piled high with metaphors and post-modernisms. He says, for instance, that the free market is “flesh-eating,” which is clearly meant as a criticism, but how exactly would things be different if the market were merely vegetarian? What does it even mean to say that we need “relief from the existential exhaustion of perpetual dynamism” engendered by the market? Before reading Reno’s piece, I had no idea I suffered from existential exhaustion; I didn’t even feel tired. Is it possible to suffer from existential exhaustion and not know it? Can two people live in the same capitalist society, with one of them being existentially exhausted by the market while other is, say, mythopoetically rejuvenated?

One of the virtues of the journal Richard John Neuhaus edited was that it was a locus of logic and clear thinking. First Things is changing in more ways than one.

Reno’s Argument

That said, as far as I can make out, Reno’s argument goes basically like this. In recent decades, we have achieved great new degrees of economic freedom through deregulation. “We do not live in a . . . regulated . . . world” any more but are “drowning in freedom.” This new freedom has greatly benefited “those who participate in the global economy” but not people who used to hold “dwindling manufacturing jobs” and find themselves displaced by new technologies. This “growing divide” threatens both democratic political institutions and Judeo-Christian morals. In particular, “because super-majorities in the West experience few impediments to earning and accumulating wealth,” “age-old expectations of marriage and children have become choices.” We want “freedom from all constraints, even those imposed by nature and our bodies,” so that “we can even choose to become male or female.” In other words, expanding economic freedom leads to transgenderism.

Even worse, “the dynamism of free market capitalism invades … and sometimes destroys” such important things as “belonging to a family,” “participating in civic culture,” and “being in solidarity as a distinct people that shares a common future, the most important of which is the Church.” Capitalism makes us neglect the human need for “ends, purposes, and projects to which we can entrust our loyalty,” with the result that nowadays “we need clarity about the ends economic freedom should serve: the renewal of marital stability and fruitfulness, the restoration of democratic institutions,” and the pursuit of “higher things than can be had in any market.”

Practically every bit of this is wrong. Let’s start with the first claim—that we have much more economic freedom today than a few decades ago because there is much less government regulation of the economy now than in the past. My apologies to Reno, but, as an empirical claim about the state of the world, this is quite absurd. There are serious people in the world who study the quantity and effects of economic regulation in rigorous ways, and none of them think there is substantially less economic regulation now than a few decades ago. On the contrary, the trend is wholly in the other direction.

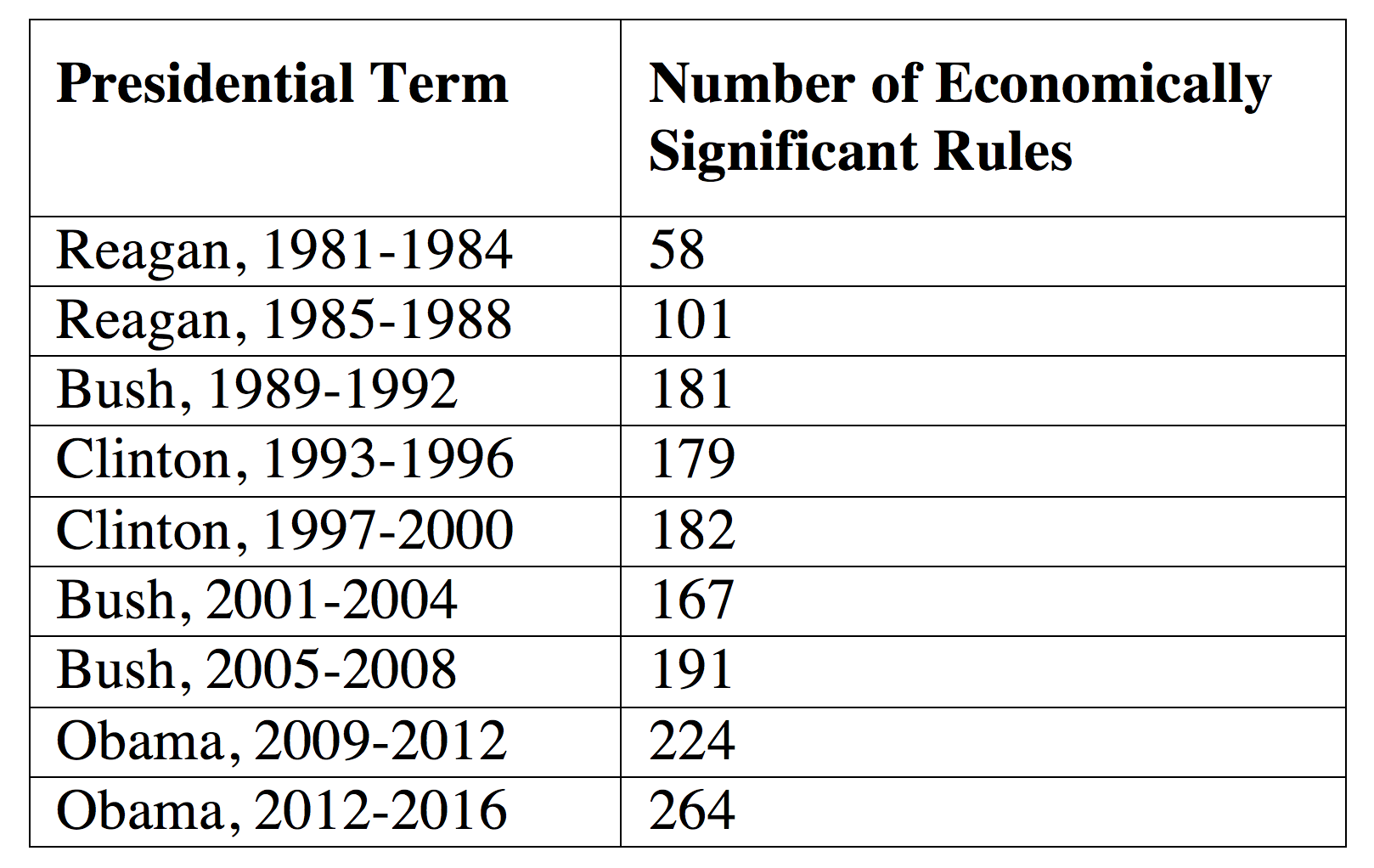

Some of the simpler metrics used in the scholarly literature include the number of pages published annually in the Federal Register (about 20,000 in 1970, but more than 90,000 in 2016) and the number of pages in the Code of Federal Regulations (fewer than 60,000 in 1970, but more than 180,000 in 2016). More sophisticated measures, which attempt to take account of the economic effects of regulations, tell the same story. Under Executive Order No. 12866, an “economically significant rule” is, basically, one that costs the economy at least $100 million per year. Consider the number of economically significant rules issued by executive agencies since 1981 (all figures derive from data published by the Regulatory Studies Center at George Washington University):

The trend is unequivocal. The academic literature on regulation entirely refutes Reno’s claim.

But resorting to such literature is supererogatory, for surely everyone knows that, merely during the Obama Administration, we got such immense new regulations as the Dodd-Frank Wall Street Reform and Consumer Protection Act, which involved the promulgation of hundreds of new financial regulations and created two new regulatory agencies (the Financial Stability Oversight Council and the Consumer Financial Protection Bureau), and the Patient Protection and Affordable Care Act, which regulated virtually all aspects of consumer health insurance. The Obama Administration also gave us the Clean Power Plan to reduce global warming, the Net Neutrality Rules to regulate internet pricing, and the Waters of the United States (WOTUS) regulation, which literally allows the Environmental Protection Agency to regulate drainage ditches and dry creek beds as “navigable” waters.

Or, to take another example, in the 1950s less than 5% of the workforce worked in jobs covered by state occupational licensing laws, but nowadays that figure is over 30% (see this paper by Kleiner and Krueger). In some states, you need a license from the government even to be an interior decorator. Such depressing examples can be multiplied almost without limit.

The Glass-Steagall Act

Confronted with such evidence, Reno has discovered a new argument. He notes that the Glass-Steagall Act of 1933 was repealed in 1999 by the Gramm-Leach-Bliley Act, and he argues that Glass-Steagall was a draconian regulation that “separated commercial from investment banking” and “prevented Wall Street from using the largest source of available capital (bank deposits) to make markets.” When Glass-Steagall was repealed, there may have been a bunch of new regulations swelling the statute books to limit how Wall Street used bank deposits, but the overall effect was much more economic freedom.

To Reno, this is a very penetrating bit of discourse. To me, it’s yet another urban legend about Glass-Steagall. Usually the claim is that repealing Glass-Steagall caused the financial crisis of 2007-2008. That’s a pretty silly idea (see Gorton, Getting Up to Speed on the Financial Crisis), but it has some surface plausibility: after all, Glass-Steagall was a banking regulation, and the financial crisis involved banks. But let us give credit where credit is due: Seeing further than all the other Glass-Steagallists, Reno has secured his place in history by discovering that the true origin of the transgender movement lies in combining commercial and investment banking.

But seriously, as to the relation of Glass-Steagall and economic freedom, recall that Glass-Steagall concerned banking, which is only part of the much larger financial sector (think of insurance, securities and commodities exchanges, regulation of public companies, and so on), and the financial sector is only part of the much larger total economy. Whatever you may think about Glass-Steagall, most economic regulation concerns the approximately 90 percent of the economy that is not the banking sector. Of the fifty titles in the Code of Federal Regulations, only one, Title 12, concerns banking. Here are some of the others, along with data about how the length of such regulations has increased between 1970 and 2017 (or other dates, as noted):

No matter what happened with Glass-Steagall, virtually every other sector of the economy has become much more regulated since 1970. That point, standing alone, is sufficient to knock the bottom out of Reno’s larger argument about economic freedom.

But Reno is wrong about Glass-Steagall too. Glass-Steagall, technically known as the Banking Act of 1933, was a result of the rolling bank failures of 1931-1932 at the beginning of the Great Depression. Indeed, it was one of many new financial regulations enacted at the time, such as the Securities Act of 1933 and the Securities Exchange Act of 1934. As Reno says, the act required banks to choose to be either commercial banks, which accept deposits from consumers and lend to individuals and businesses, or investment banks, which underwrite and deal in securities. The theory behind Glass-Steagall was that commercial banking was less risky than investment banking, and so separating the two would protect consumers from a bank taking their deposits and then going bankrupt speculating on securities. Since Glass-Steagall also created the Federal Deposit Insurance Corporation (FDIC) to insure deposits at commercial banks, in protecting consumers the act would also protect the public fisc.

The New Deal system of banking regulation remained stable until about 1980, when what is usually regarded as a slow-motion revolution in the financial industry began. On the one hand, this revolution involved some deregulating of the financial sector, including not only the repeal of Glass-Steagall but also deregulation of deposit interest rates (older regulations had prohibited banks from paying interest on deposits) and the removal of geographical restrictions on banks. On the other hand, the revolution also involved significant new forms of regulation, including massively complicated capital regulations (Basel I, Basel II, and Basel III) and many new forms of consumer protection regulation, including regulations under the Community Reinvestment Act of 1977, the Right to Financial Privacy Act of 1978, the Expedited Funds Availability Act of 1987, the Truth in Savings Act of 1991, and the Credit CARD Act of 2009.

Hence, as I said in my prior go-around with Reno, the financial sector is more free in some respects and less free in others than it was in the past. The net effect is difficult to estimate, but here’s one way of trying: the Heritage Foundation/Wall Street Journal Index of Economic Freedom includes a component measuring financial freedom, and it held steady from 1995 (the first year the index was computed) until 1999, when Glass-Steagall was repealed; it then spiked upwards, but by 2010 it had fallen back to the 1995-1999 level. That sounds about right to me.

But Reno misses the really important point, which is that the revolution in the financial sector was not primarily about either regulation or deregulation. As the authors of a leading reference work on financial regulation put it, “the banking revolution has, above all, occurred outside the legal system through fast-paced market developments.” The relation of commercial and investment banking is a good example. Long before 1999, people began to realize that, although there are benefits to separating commercial and investment banking (mostly in the form of specialization, including regulatory specialization), there are also significant costs. Besides losing synergies that could be captured by combining different kinds of financial businesses, Glass-Steagall’s basic theory about risk was probably wrong. It’s counterintuitive, but there are reasons to think that commercial banking may be riskier than investment banking, and, in any case, because of the risk-reducing effects of diversification, a business engaged in both commercial and investment banking may be less risky than one engaged in commercial banking only.

For reasons like these, commercial banks had moved into investment banking long before the repeal of Glass-Steagall. This was possible because, even under Glass-Steagall, the separation between commercial and investment banking was never absolute, and by 1999 the Federal Reserve had granted at least 51 so-called “Section 20 exceptions” allowing commercial banks to have affiliates involved in the securities business. Moreover, even after the repeal of Glass-Steagall, a bank engaging in both commercial and investment banking must hold its FDIC-insured deposits in a separate subsidiary meeting a host of capitalization, management, and other requirements. All things considered, the effect of repealing Glass-Steagall was small compared to the effects of market forces that were driving commercial banks into the investment banking business.

So is Reno right that the immense increase in the length of the banking regulations in recent decades resulted from the repeal of Glass-Steagall? No, he’s not. In 1999, before the repeal, the banking regulations in Title 12 contained 3,229 pages. Four years later in 2003, when all important regulations replacing Glass-Steagall had been promulgated, Title 12 contained 3,918 pages, an increase of 689 pages. For the sake of argument, assume all 689 of those pages were replacing Glass-Steagall. Nevertheless, Title 12 expanded from 987 pages in 1970 to 9,134 pages in 2017, which means that there were at least 7,458 new pages of banking regulations unrelated to the repeal of Glass-Steagall. Most of these concern the capitalization requirements and the consumer-protection regulations I mentioned above.

But Reno is a big-picture guy, so maybe he’s right on the big issue—that repealing Glass-Steagall let Wall Street access bank deposits, “the largest source of available capital,” which the investment banks then used to deal in securities, presumably with dreadful consequences for everyone else. But Reno is not right here; in fact, he’s even more wrong than usual. When Glass-Steagall was repealed, none of the major investment banks—not one—elected to enter the commercial banking business. Nor was this surprising, for, contrary to Reno’s assertion, consumer deposits are not the largest source of available capital. For example, in 1999, bank deposits in the United States totaled $5.2 trillion, which was only about a third of the $15.3 trillion invested in the bond market at the time. By 2015, bank deposits were even less important: they amounted to only about a quarter of the bond market, or $9.9 trillion compared to $38.2 trillion. Moreover, it’s not just the size of a potential funding source that matters; it’s also the cost of accessing it. Taking deposits from consumers is an expensive way of borrowing money because, although you pay very little in interest, you have to maintain thousands of bank branches and pay tens of thousands of employees to work in them. If all you want to do is borrow money, it’s much cheaper to access capital markets directly, borrowing long-term in the bond market or short-term in the commercial paper or repo markets, which is how investment banks typically fund their activities.

So the conclusion remains that, contrary to Reno’s assertion, the economy is much more regulated, and thus much less free, than it was two generations ago. Strictly speaking, with its major factual premise false, the rest of Reno’s argument collapses. Still, there are some instructive errors in the other steps of that argument, and I shall consider some of these tomorrow.